Many Florida homes sit in special flood hazard areas. If you find the right house and then learn it is in a high-risk flood zone, the next questions are practical: what does that mean for insurance, monthly payment, and mortgage approval?

Here in Boca Raton flooding is a constant issue since we live so close to the beach and can get hit hard with hurricane rains. In this article, I will go over the different types of flood zones and how they can impact your home buying process. Along with some pros and cons of buying in a flood zone.

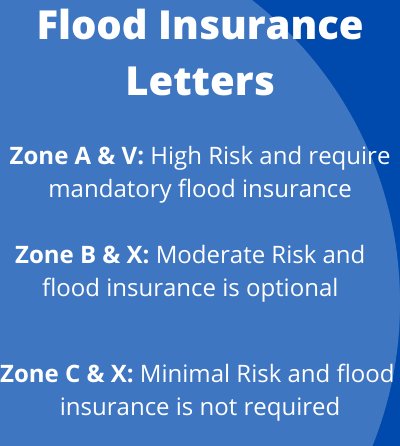

Flood Zone Letter Codes

Flood zone letter codes help identify the level of flood risk for a property. The full list can be confusing, but the first letter usually tells you whether the home is in a high-risk, moderate-risk, or lower-risk area.

Being in the high-risk zone generally means your lender will require flood insurance with your mortgage. For a newer mortgage-specific checklist, see MJS Financial’s guide to Florida flood insurance and mortgage approval. Moderate risk areas have a 0.2-percent-annual-chance of flooding. Minimal risk areas are like moderate risk areas but are higher in elevation. To know which zone a house is in you can contact the zoning department of a city or go online to the FEMA website.

Pros and Cons Of Buying In A Flood Zone

Pros:

-Houses in flood zones tend to be closer to water.

-Negotiation leverage

-House might be cheaper

Cons:

-Risk of house getting flooded and having flood damage.

-Monthly flood insurance

It is important to note that flood zones change every year and just because your house is not in a flood zone means there are zero risks. A perfect example is when hurricane Harvey hit Houston and a lot of houses that were not in flood zones getting damaged with many homeowners not having flood insurance.

Flood Insurance And Mortgages

If you are buying a house in flood zone A or V, your lender may require flood insurance before closing. Many borrowers use a National Flood Insurance Program (NFIP) policy, while others compare private flood insurance options. Either way, the policy has to satisfy the mortgage lender before the loan can close.

Buying In A Flood Zone

Before committing to buying the house take some time and speak with the current owner, real estate agent, or any friends and family you might have that live in a flood zone.

Speak with the homeowner and see how long they have been living there, what insurance do they have, and what storms or events cause any damage if any. Speak to your real estate agent they see so many houses per day that they have almost seen it all. They should be able to tell you based on location what risks are present and how often it might flood based on the bodies of water nearby. Lastly speaking with friends and families who live in flood zones to get their opinions if they think it’s a big risk or if they do not mind living in that area.